Headline: Flash! Container Freight Rates Soar as Red Sea-Driven Momentum Weakens

Source: 5688.cn

Near the Cape of Good Hope in Africa, a significant number of container ships changing course has led to a surge in spot prices, but the impact from the Red Sea may have reached its limit.

The upward momentum has weakened, with rates stabilizing in most lanes, and several major European indices have experienced a downturn.

For the week ending last Friday, the Shanghai Containerized Freight Index (SCFI) recorded a 2.7% decline compared to the previous week, marking the first weekly decrease since late November of the previous year.

Oar Nokta, a shipping analyst at Jefferies, stated on Friday, "Pressure on freight rates into Europe continues to ease from the highs, but rates remain robust in other regions."

The current rate dynamics are different from those during the pandemic boom. The supply chain crisis from 2020 to 2022 was demand-driven as consumers purchased more goods during the pandemic. The current rate surge is supply-driven.

The rerouting of vessels near the Cape of Good Hope has extended transit times, occupying the supply of vessels and container equipment. However, as routes adjust to longer paths, theoretically, rates should stop rising, curbing higher demand.

The record number of new ships that container shipping companies received this year should provide them with more vessel supply to handle longer routes. Additionally, the Chinese New Year holiday in early February is expected to temporarily limit ship demand, alleviating supply tightness.

Lars Jensen, CEO of consultancy firm Vespucci Maritime, wrote in an online post, "Once past the Chinese New Year, not only will demand decrease, giving us some breathing room, but we will also start to see the movement of vessels and equipment on the new around-Africa routes entering predictable patterns."

"This still means rates will be far higher than pre-crisis levels, as longer routes consume a lot of capacity and incur additional costs, but I expect the surge in spot rates to weaken. On the other hand, contract rates may rise, as in the foreseeable future, we seem to be entering an around-Africa (pattern).

The impact on the contract market is reflected in the China Containerized Freight Index (CCFI), which, unlike SCFI, includes contract rates. While the SCFI index fell this week, the CCFI index rose by 9%.

Regarding spot rates, Platts, a subsidiary of S&P Global (NYSE: SPGI), has assessed that spot rates have peaked.

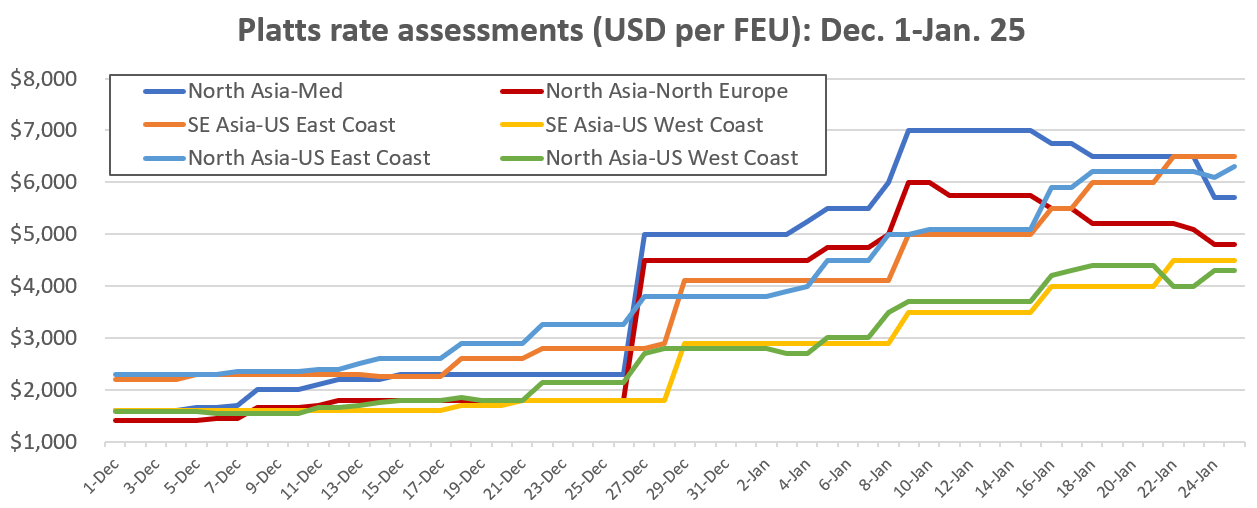

Platts Energy Information reported on Thursday that the spot rate for North Asia to the Mediterranean was $5,700 per 40-foot equivalent unit (FEU), down 19% from the peak reached between January 9 and 15. The assessment for North Asia to Northern Europe was $4,800 per FEU, a 20% decrease from the high on January 9 and 10.

In contrast, rates in the U.S. import corridors are still at their highest levels, although the rate of increase has slowed.

Platts Energy Information on Thursday set the Southeast Asia to U.S. East Coast rate at $6,500 per FEU, up 195% since December 1; North Asia to U.S. East Coast rates were $6,300 per FEU, up 174%; Southeast Asia to U.S. West Coast rates were $4,500 per FEU, up 181%; and Southeast Asia to U.S. East Coast rates were $4,300, up 173%.

FreightWaves data based on Platts Energy Information

Drewry World Container Index (WCI)

The Drewry World Container Index (WCI) shows that rates are still rising, albeit at a much slower pace in the European market.

For the week ending Thursday, the WCI global index increased by 5% compared to the previous week. The Shanghai to Rotterdam index was $4,984 per FEU, with a weekly increase of only 1%. The average spot rate from Shanghai to Genoa, Italy, was $6,365 per FEU, also rising by 1%.

In contrast, the WCI Shanghai to Los Angeles index increased by 13% to $4,344 per FEU, and the Shanghai to New York index increased by 9% to $6,143 per FEU.

Baltic Freight Index (FBX)

The Baltic Freight Daily Index (FBX) global composite index reported $3,409 per FEU on Thursday, remaining flat since Monday.

The FBX China to Mediterranean rate was $6,403 per FEU, down 8% from the peak reached on January 18. The China to Northern Europe rate was $5,366 per FEU, a 7% decrease from January 18.

The China to U.S. East Coast rate remains at its highest level since the Red Sea crisis, standing at $6,142 per FEU on Thursday, unchanged since Monday, but up 143% since December 1.

The China to U.S. West Coast rate continues to rise, reaching a peak of $4,198 per FEU on Thursday, up 169% since December 1.

Disclaimer: This message has been reprinted from other media, and its publication is for the purpose of conveying more information, and does not imply agreement with its views or confirmation of its description. The content of the article is for reference only and does not constitute any suggestions.

Copyright ©2023 MASTER INTERNATIONAL LOGISTICS Co., Ltd |

|

Tel:86–21–61420605

Tel:86–21–61420605 Fax:86–21–61420605

Fax:86–21–61420605 Email:keven_yang@master-log.com

Email:keven_yang@master-log.com